Financial statements provide insight into a company’s well-being, often hard to assess through other methods. Although accountants and finance experts are skilled at interpreting these documents, many business professionals may find them confusing. This can lead to important information being unclear.

To grasp a company’s financial status, it’s essential to examine various statements. In this article, we are going to dive deep into decoding the balance sheet.

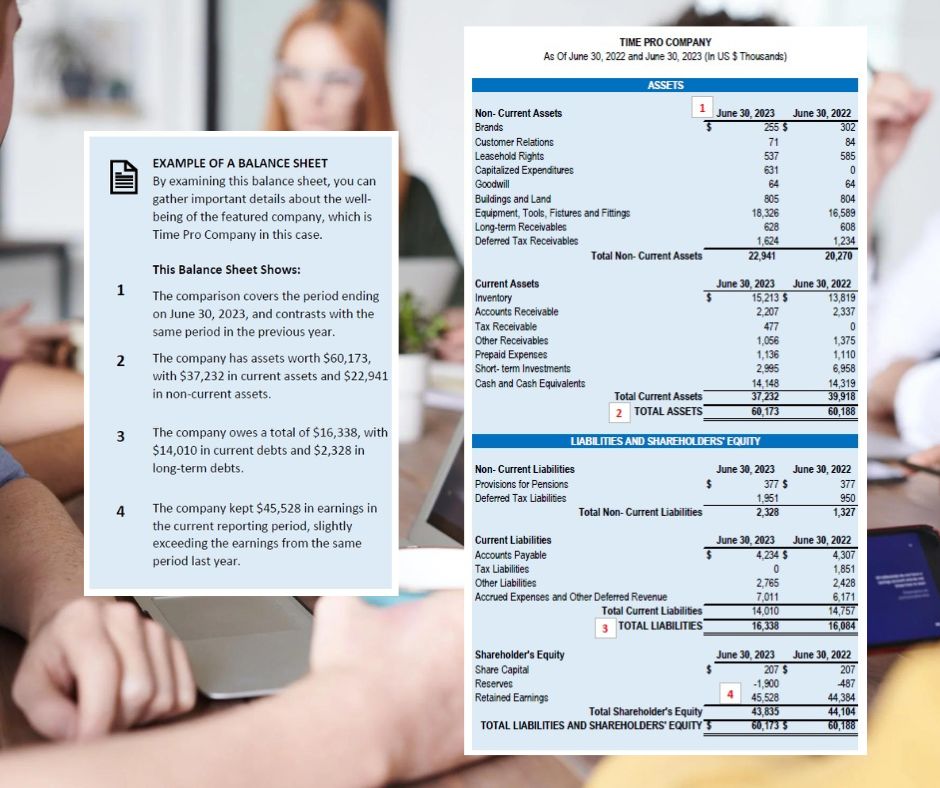

The Balance Sheet

A balance sheet is a financial report that shows the value of a company or organization, known as its “book value.” It does this by listing and adding up all the assets, liabilities, and owner’s equity as of a specific reporting date. Normally, companies create and share balance sheets every quarter or month, following legal requirements or company rules.

Essential Functionality of a Balance Sheet

Balance sheets serve two distinct purposes, depending on who is looking at them.

Internally, a company examines its balance sheet to understand if the company is doing well or facing challenges. This helps in adjusting strategies: reinforcing successful aspects, correcting shortcomings, and exploring new opportunities.

Externally, when outsiders like potential investors or auditors review a balance sheet, the focus is on understanding a business’s available resources and how they were funded. This information guides investors in deciding whether to invest and helps auditors ensure that the company complies with reporting laws.

It’s crucial to note that a balance sheet reflects information as of a specific date and is based on past data. Although investors may use it to predict future performance, past success does not guarantee future results.

What’s in a Balance Sheet?

Balance sheets typically organize information based on the accounting equation:

Assets = Liabilities + Owners’ Equity

Although this equation is widely used, there are alternative ways of organizing the information, and here are some other equations you might come across:

Owner’s Equity = Assets – Liabilities

Liabilities = Assets – Owner’s Equity

A balance sheet must always be in balance, meaning that assets should equal liabilities plus owners’ equity. There may be errors in the document preparation if disbalances appear in the equation. Errors can arise from incomplete or missing data, incorrectly entered transactions, inaccurate currency exchange rates or inventory levels, mistakes in calculating equity, or errors in depreciation or amortization calculations.

The balance sheet consists of three main components: assets, liabilities, and owners’ equity.

Assets

An asset is something a company owns that has measurable value. If needed, a business can turn an asset into cash through liquidation. Assets are usually listed as positives (+) on a balance sheet and categorized as current assets or non-current assets.

Current assets are items a company anticipates converting into cash within a year, like:

- Cash and cash equivalents

- Prepaid expenses

- Inventory

- Marketable securities

- Accounts receivable

Non-current assets usually consist of long-term investments that are not anticipated to be converted into cash shortly, such as:

- Land

- Patents

- Trademarks

- Brands

- Goodwill

- Intellectual property

- Equipment (used to produce goods or perform services)

Companies invest in assets to achieve their goals. It’s crucial to have a clear grasp of these investments to comprehend financial documents like the balance sheet, which reflect a company’s overall well-being. Without this understanding, interpreting such documents can be difficult.

Liabilities

A liability is the opposite of an asset, these are things a company owes. Financial and legal obligations typically appear negative (-) on a balance sheet.

In this portion, we also sorted liabilities in the same manner: current or non-current categories.

Current liabilities usually involve amounts that need to be paid within a year and may include:

- Payroll expenses

- Rent payments

- Utility payments

- Debt financing

- Accounts payable

- Other accrued expenses

Non-current liabilities generally encompass long-term obligations or debts that are not expected to be due within the next year. Examples may include:

- Leases

- Loans

- Bonds payable

- Provisions for pensions

- Deferred tax liabilities

Liabilities can also involve a commitment to offer goods or services later on.

Owner’s Equity

Owners’ equity, or shareholders’ equity, is what belongs to business owners after considering all debts. It’s the leftover value when you subtract what a business owns (assets) from what it owes to others (liabilities).

Owners’ equity has two main parts. The first part is the money. Investors put money into the business as an investment, and they often represent it with shares. Second, it includes the profits the company makes and keeps over time.

Final Thoughts

Understanding a financial statement might seem complex to some. We aim to make it easier by breaking down the key elements of a balance sheet in this guide. Keep in mind, though, that a financial statement includes other parts such as the Income Statement, Cashflow Statement, and Annual Report.