Any given finance professional will be cognizant of the significance of the cash flow statement. However, not everyone is well versed in the best practices in the creation of such statements. Maximizing such statements requires a proficient understanding in a few critical aspects of the art of the cash flow. These aspects include:

- Proper Organization

- Correctly Classifying Different Cash Flow Statements

- Conducting Proper Calculations and Analyses

- Understanding the Appropriate Resources for Cash Flow Statements

Cultivating a thorough understanding of how to best create cash flow statements can greatly benefit a finance team, as such statements are an integral part of corporate finance.

Defining Cash Flows & Proper Organization

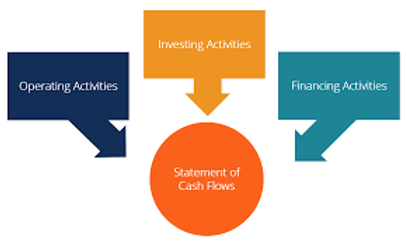

The Statement of Cash Flows (also referred to as the cash flow statement) is one of the three key financial statements (the others being the income statement and the balance sheet) that report the cash generated and spent during a specific period of time (i.e. a month, quarter, or year). The statement of cash flows serves as a bridge between the balance sheet and income statement by how money has moved in and out of the business.

Three main sections of Statement of Cash Flows:

- Financing Activities: Any cash flows that result in changes in the size and composition of the contributed equity and borrowings of the entity (i.e. bonds, stock, cash dividends)

- Operating Activities: The principal revenue-generating activities of an organization and other activities that are not investing or financing; any cash flows from current assets and current liabilities

- Investing Activities: Any cash flows from the acquisition and disposal of long-term assets and other investments not included in cash equivalents

Cash Flow Classifications

1. Operating Cash Flow: Operating activities are the principal revenue-producing activities of the entity. Cash Flow from Operations typically includes the cash flows associated with sales, purchases, and other expenses. The company’s chief financial officer (CFO) chooses between the direct and indirect presentation of operating cash flow. The latter is specifically referred to as the “cashflow indirect method” in Excel.

2. Direct Presentation: Operating cash flows are presented as a list of cash flows; cash in from sales, cash out for capital expenditures, etc. This is a simple but rarely used method, as the indirect presentation is more common.

3. Indirect Presentation: Operating cash flows are presented as a reconciliation from profit to cash flow. The items in the cash flow statement are not all actual cash flows, but “reasons why cash flow is different from profit.”

Depreciation expense reduces profit but does not impact cash flow (it is a non-cash expense). Hence, it is added back. Similarly, if the starting point profit is above interest and tax in the income statement, then interest and tax cash flows will need to be deducted if they are to be treated as operating cash flows.

There is no specific guidance on which profit amount should be used in the reconciliation. Different companies use operating profit, profit before tax, profit after tax, or net income. Clearly, the exact starting point for the reconciliation will determine the exact adjustments made to get down to an operating cash flow number.

(Example Cash Flow Statement, including info regarding depreciation, net income, etc)

Investing Cash Flow

Cash flow from investing activities includes the acquisition and disposal of non-current assets and other investments not included in cash equivalents. Investing cash flows typically include the cash flows associated with buying or selling property, plant, and equipment (PP&E), other non-current assets, and other financial assets. Cash spent on purchasing PP&E is called capital expenditures (CapEx).

Financing Cash Flow

Cash flow from financing activities are activities that result in changes in the size and composition of the equity capital or borrowings of the entity. Financing cash flows typically include cash flows associated with borrowing and repaying bank loans, and issuing and buying back shares. The payment of a dividend is also treated as a financing cash flow.

Best Practices In Creating An Effective Cash Flow Statement

1. Understand Direct vs. Indirect Methods:

The operating section of the statement of cash flows can be shown through either the direct method or the indirect method. With either method, the investing and financing sections are identical; the only difference is in the operating section. The direct method shows the major classes of gross cash receipts and gross cash payments. The indirect method, on the other hand, starts with the net income and adjusts the profit/loss by the effects of the transactions. In the end, cash flows from the operating section will give the same result whether under the direct or indirect approach, however, the presentation will differ.

The International Accounting Standards Board (IASB) favors the direct method of reporting because it provides more useful information than the indirect method. However, it is believed that greater than 90% of public companies use the indirect method. The following illustrates a comparison the two cash flow statement methods:

2. Calculate the Cash Coming in (Sources of Cash)

Figure out all the money you expect to take in during the month. Only include actual money you will be receiving, not the sales you have made. For example, if you signed a contract for $100,000 over the next six months but are only receiving $15,000 of it this month, you would only count $15,000 for now because that would be the cash you have on hand.

Count everything coming in, including all collections of previous sales you made on credit, any transfers of your own personal money into the business, and any loans you might have taken during the period. Basically, you will include every single dollar coming into your business, whether from operations (sales of your goods or services), investments (sales of assets such as business equipment or land), or financing activities (equity you and/or shareholders are providing, or loans).

Add the figure you’ve arrived at in Step 2 to your opening balance from Step 1 to get your total cash balance for the period.

3. Determine the Cash Going Out (Uses of Cash)

Now, count up and enter all of the payments you expect to make for the month. Include items such as inventory, rent, salaries, taxes, loan payments, etc. Take into account everything you’ll spend money on this month.

If you have an annual bill for something like insurance, but have to pay for it all at one time or twice a year, you would count the payment as an expenditure during the month(s) in which you pay it. (You should still budget for it monthly, but you’ll have to come up with the cash during the month it’s actually due.)

4. Subtract Uses of Cash (Step 3) from your Cash Balance (sum of Steps 1 and 2)

The number you’re left with will be how much cash you have left at the end of the month. It will also be your Opening Balance at the start of the next month. If the number is negative, it means you will have a shortfall-not enough cash to cover your expenses.

Advantages of Effective Cash Flow Statements

The biggest benefit to analyzing your cash flow is the information it provides about how to handle your expenses. While your business may be profitable in the long run, you may still have periods where you don’t have the money to pay your bills. This is especially true for companies that do a lot of invoicing.

Not all customers pay on time, and sometimes, they don’t pay at all. Because cash flow ONLY counts the money you’ve actually received, it can be more realistic than your profit and loss statement when it comes to figuring out the financials of your operation.

When you see the figures in black and white, you’ll realize the periods in which you either have to cut the amount of money you’re spending or increase the money coming in-whether it’s by booking more business, getting paid faster, or getting a loan or a line of credit.

Tools Used For Cash Flow Statements

Microsoft Excel for years has proved to be an effective tool in creating cash flow statements. One of Excel’s best features is its templates designed for cash flow statements. This is the best manual method for this task. However, the proliferation of technologies like financial software has enabled many finance teams to automate their cash flow statements.